Tutorial 2: the Solow model

We are going to dig into into the seminal model of growth theory in macroeconomics: the Solow model.

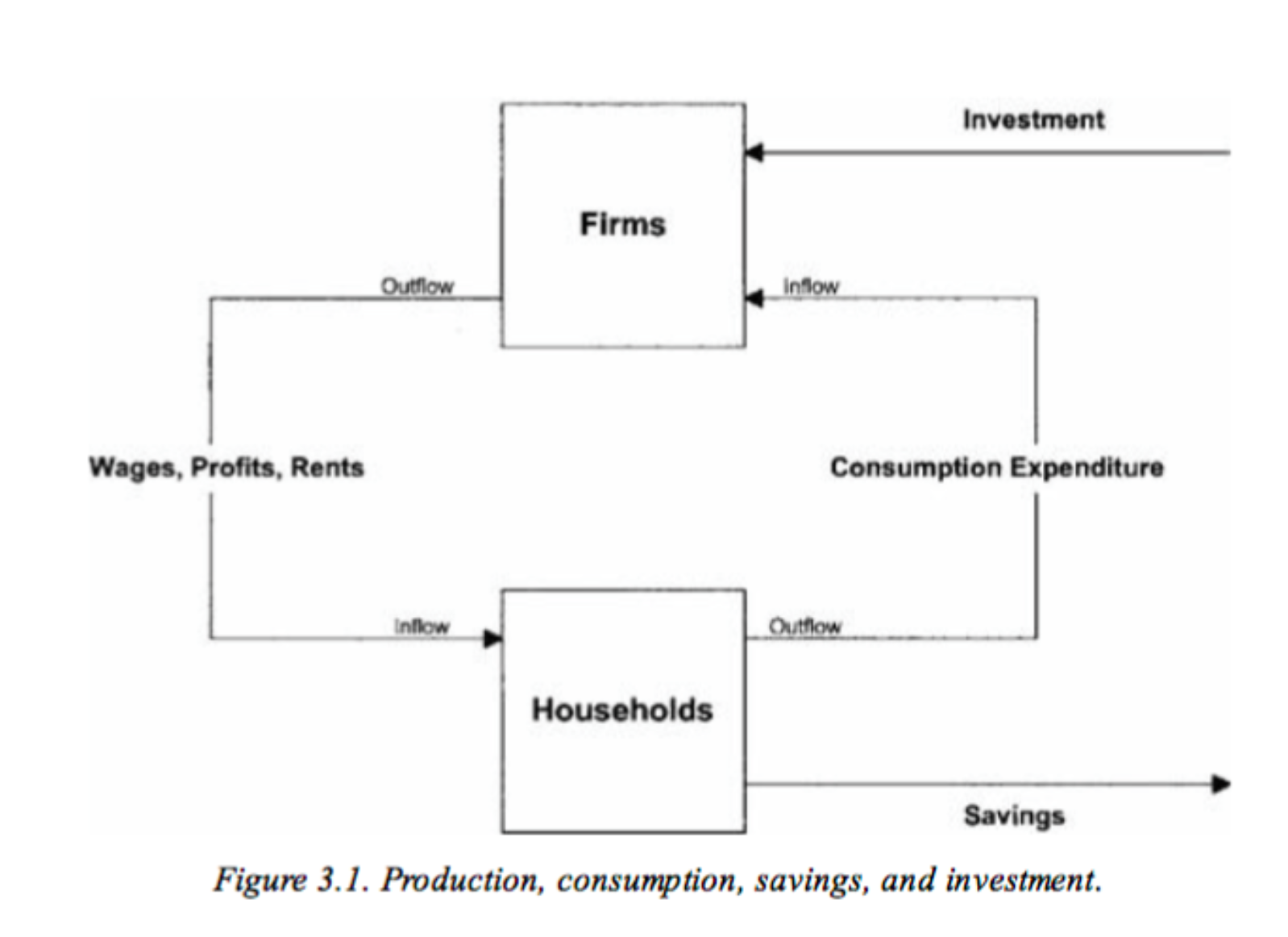

Quick model summary

Structure of the economy: firms and consumers (no state). Firms use (and pay) capital and labor to produce an output. Output (=income) is either consumed or saved by households:

\[ Y_t = C_t + I_t \]

Production Function: a representative firm produces output using a Cobb-Douglas production function: \[ Y_t = F(K_t, A_tL_t) = K_t^\alpha (A_tL_t)^{1-\alpha}\] where \(Y\) is output, \(K\) is capital, \(L\) is labor and \(A\) is technology. where \(0 < \alpha < 1\). Using capital comes at rental price \(r\) and labor comes at price \(w\) (the wage).

Capital accumulation: capital accumulates through savings and depreciates geometrically

\[ K_{t+1} = I_t + (1-\delta) K_t\]

Saving rate: investment is a constant fraction of output

\[ I_{t} = sF(K_t,A_tL_t)\]

Definitions

- Steady state: trajectory where all variables are constant

- Balanced growth path: trajectory such that per capita variables grow at a constant rate (not necessarily the same) and the capital to output ratio is constant

Exercise

1. Warm-up: Return to scale

Let \(\lambda > 1\), if \(F(\lambda X, \lambda Y) < \lambda F(X,Y)\), the function has decreasing return to scales (and increasing for \(>\)). If \(F(\lambda X, \lambda Y) = \lambda F(X,Y)\), the function has constant return to scale. For the following functions, state if they exhibit positive, constant, or negative return to scale.

- \(y_1 = 10x^2y^2\)

- \(y_2 = \frac{1}{2}x^{1/3}y^{1/2}\)

- \(y_3 = x + 2y\)

- \(y_4 = \ln(xy)\)

2. Solve the firm’s maximization problem

Consider the function above (\(Y_t = K_t^{\alpha} (A_tL_t)^{1-\alpha}\)).

- Show that if \(K=0\) and/or \(L=0\) production does not occur

- Show that the production function has constant return to scale

- Show that marginal productivity is positive for capital and labour

- Show that marginal productivity is decreasing for capital and labour

- Write the down the profit maximization program (maximizing profit with respect to K and L) and derive its first order conditions

- Show that all output is needed to pay capital and labor

3. Constant population and technology

For now, we consider that technology and labor (=population) are constant (\(A_t = A\), \(L_t = L\)): no population growth, no technological progress.

- Using the capital accumulation equation, show that the ratio \(\frac{K_{t+1}}{K_t}\) goes to \(\infty\) as \(K_t\) goes to 0 and is lower than 1 when \(K_t\) goes to \(\infty\)

- Show that there is a unique steady state level of capital \(k^*\) and solve for it

- How does the \(k^*\) vary with \(s\), \(\delta\), \(A\), \(L\) ? Interpret

4. Population and technology growth

We now assume that population grows at constant rate \(n\), and technology at rate \(g\):

\[L_{t+1} = (1+n) L_t\]

\[A_{t+1} = (1+g) A_t\]

We respectively denote \(y_t=Y_t/L_t\) and \(k_t=K_t/L_t\), the per-worker production and capital

We further define \(\hat{y_t}=\frac{Y_t}{A_t L_t}\) and \(\hat{k_t}=\frac{K_t}{A_tL_t}\) the production and capital per effective unit

Dividing the capital accumulation equation by \(A_tL_t\), show that

\[\hat{k_{t+1}} (1+n)(1+g)= (1-\delta)\hat{k_t} + s F(\frac{K_t}{A_tL_t},1)\]

Show that there is a steady state level of capital per effective unit \(\hat{k^*}\) equal to:

\[ \hat{k^*} = \left(\frac{s}{(1+n)(1+g)-1+\delta}\right)^{\frac{1}{1-\alpha}} \]

- Show that per capita outcomes \(y\) and \(k\) are on a balanced growth path. What is their respective growth rates?

5. Discussion

- What makes this model a simplification of reality?

- Why cannot it explain all differences in output growth and per capita level across economies?